Comments

More from Hayden Otto

Sam Bankman-Fried’s Alameda Research & FTX Insolvent - Here's Why

It’s looking increasingly likely that Sam Bankman-Fried’s trading firm, Alameda Research, is in massive financial trouble which

6 min read

How to Buy Bitcoin for Beginners – Safe and Fast!

I hear it all the time. Someone is interested in buying their first Bitcoins, but they don’t have a

5 min read

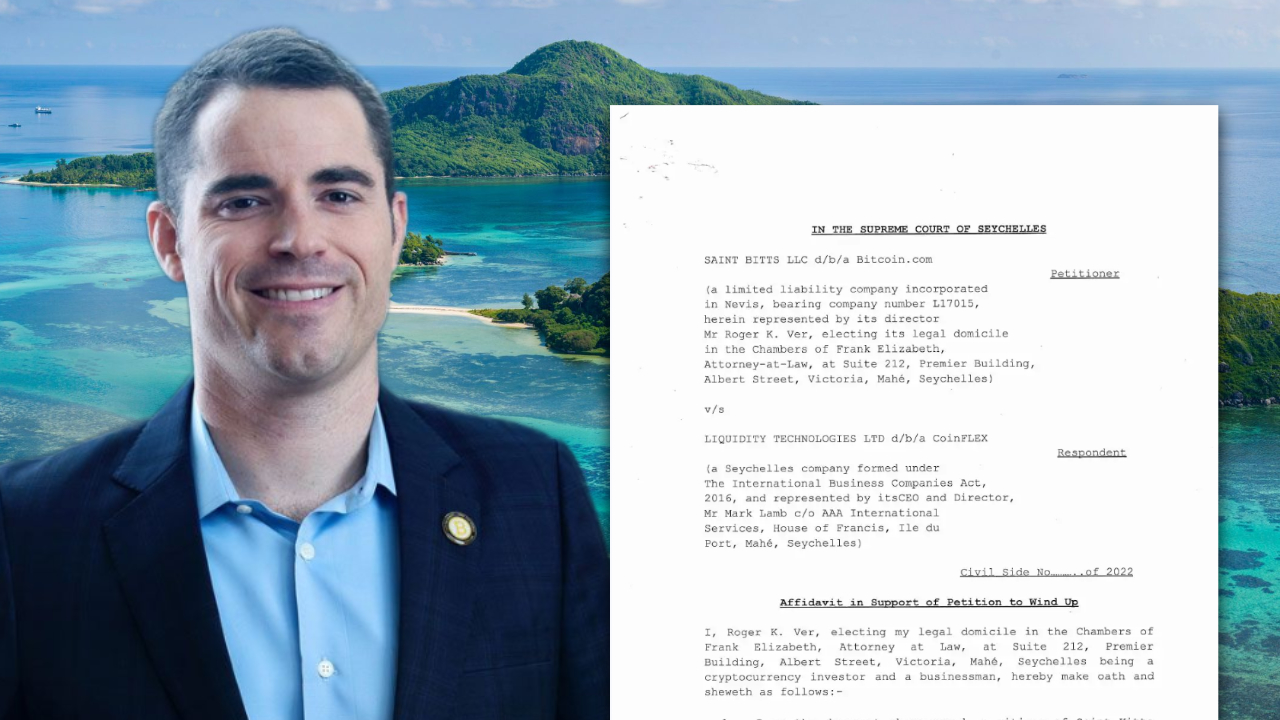

New CoinFlex Revelations as Roger Ver Strikes Back

Today new revelations emerge from the CoinFlex v Roger Ver saga, as Roger Ver’s Bitcoin.com filed a petition

1 min read